TauricResearch/TradingAgents

Wall Street roleplay for language models

A research framework that assigns LLMs to trading-floor roles—analyst, researcher, trader, risk manager—to debate and execute simulated stock decisions.

Feature · 12 Jun 2026

Wall Street Cosplay for LLMs: Why TradingAgents Went Viral

A UCLA-MIT research project turned open-source framework simulates the hierarchy of a trading floor with specialized AI agents, sparking debate about whether multi-agent theater improves returns or just adds plausible deniability to bad bets.

Read the in-depth article →

Velocity · 7d

+135

★ / day

Trend

↘cooling

star history

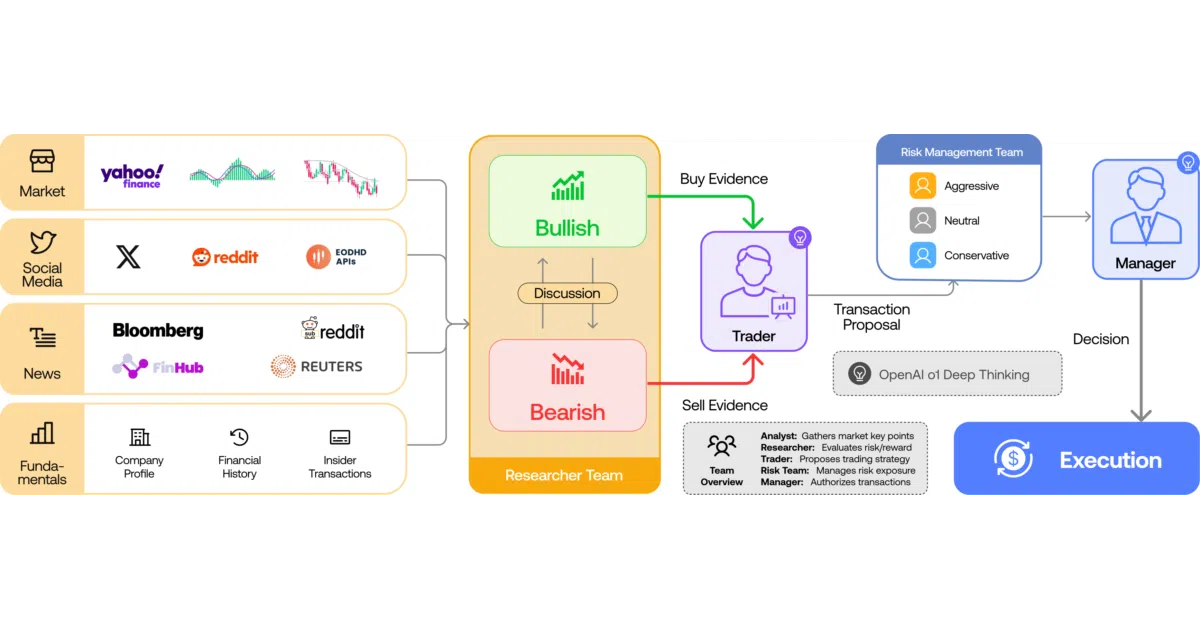

What it does TradingAgents breaks a trading decision into specialized roles handled by separate LLM agents. One cluster ingests fundamentals, sentiment, news, and technical indicators; another hosts bullish and bearish researchers who debate the findings; a trader agent synthesizes their output; and a risk-management layer plus portfolio manager signs off before a simulated exchange executes the order. The whole pipeline is wired together with LangGraph and exposed through both an interactive CLI and a Python package.

The interesting bit The framework treats disagreement as a structural feature rather than a bug: built-in bullish and bearish researchers argue over the analyst team’s output before any capital is committed. It also supports an unusually broad provider list—from OpenAI and Anthropic to Qwen, GLM, MiniMax, and local Ollama endpoints—covering both international and China-specific API regions.

Key highlights

- Multi-agent pipeline with distinct roles: fundamentals, sentiment, news, and technical analysts, debating researchers, a trader, risk manager, and portfolio manager

- Supports Yahoo Finance tickers across US, Hong Kong, Tokyo, London, India, China A-shares, and crypto markets

- Broad LLM provider support including international and Chinese endpoints (Qwen, GLM, MiniMax) plus local Ollama and enterprise Azure

- Built on LangGraph with checkpoint resume and persistent decision logs

- Runs fully offline via Ollama or remotely through cloud providers

Caveats

- The authors explicitly state the framework is for research only and not financial advice; trading performance varies wildly with model choice, temperature, and data quality

- Yahoo Finance data may be blocked or rate-limited in mainland China, though community forks target China-native sources

- The README references model versions and release dates in 2026 that appear speculative or forward-looking

Verdict Worth a look if you are building agentic workflows or researching multi-LLM decision systems. Actual traders should probably not let a committee of language models handle their real money.

Frequently asked

- What is TauricResearch/TradingAgents?

- A research framework that assigns LLMs to trading-floor roles—analyst, researcher, trader, risk manager—to debate and execute simulated stock decisions.

- Is TradingAgents open source?

- Yes — TauricResearch/TradingAgents is open source, released under the Apache-2.0 license.

- What language is TradingAgents written in?

- TauricResearch/TradingAgents is primarily written in Python.

- How popular is TradingAgents?

- TauricResearch/TradingAgents has 94.1k stars on GitHub and is currently cooling off.

- Where can I find TradingAgents?

- TauricResearch/TradingAgents is on GitHub at https://github.com/TauricResearch/TradingAgents.