TauricResearch/TradingAgents · 12 Jun 2026 · Feature

Wall Street Cosplay for LLMs: Why TradingAgents Went Viral

Amara Okonkwo

Staff Writer

A UCLA-MIT research project turned open-source framework simulates the hierarchy of a trading floor with specialized AI agents, sparking debate about whether multi-agent theater improves returns or just adds plausible deniability to bad bets.

TauricResearch/TradingAgents

★94.6k stars Velocity · 7d +135 ★/day ↘cooling

star history

The Anatomy of a Synthetic Trading Floor

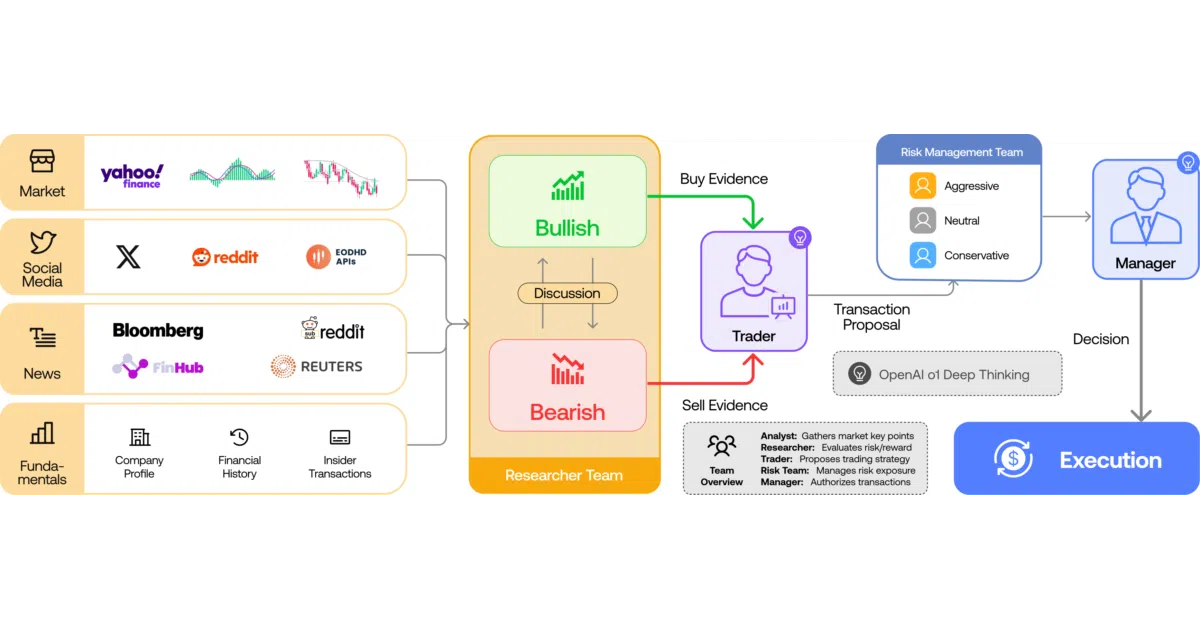

TradingAgents began as an academic exercise in organizational mimicry. Researchers at UCLA and MIT asked a simple question: if real trading firms succeed through specialization—analysts who read balance sheets, others who scan Reddit, risk officers who say no—why do most AI trading tools stuff everything into a single prompt? Their answer, published in December 2024 and revised through June 2025, is a framework that replicates the social architecture of a hedge fund using seven distinct LLM-powered roles [5][9].

The framework assigns agents to familiar Wall Street jobs. Fundamental analysts parse financial statements. Sentiment analysts scrape StockTwits and Reddit headlines. Technical analysts compute MACD and RSI. A News Analyst monitors macro events. Two Researcher agents—one bullish, one bearish—debate the synthesized findings. A Trader agent decides timing and sizing. A Risk Management team evaluates volatility and liquidity exposure. Finally, a Portfolio Manager approves or rejects the trade [3][5].

This is not merely prompt engineering with extra characters. The authors distinguish their approach from prior multi-agent systems by emphasizing structured communication protocols: concise analysis reports, decision signals, and diagrams for routine work, reserving natural language dialogue for the debate and risk-assessment phases [3]. The contrast is with frameworks that drown agents in unstructured message histories or shared data pools where context dissolves.

The Technical Guts: LangGraph and the ReAct Loop

Under the hood, TradingAgents runs on LangGraph, which provides the state-machine backbone for agent handoffs and checkpointing [README]. The framework supports a sprawling roster of LLM providers: OpenAI’s GPT-5.x family, Google’s Gemini 3.x, Anthropic’s Claude 4.x, xAI’s Grok 4.x, DeepSeek, Alibaba’s Qwen via dual-region endpoints, Zhipu’s GLM, MiniMax, OpenRouter, local Ollama instances, and Azure OpenAI for enterprise deployments [README].

The ReAct prompting framework drives agent reasoning—reasoning, acting, observing, repeating [3]. Agents do not merely generate text; they generate structured outputs that feed into downstream nodes. The framework’s v0.2.4 release added structured-output agents for the Research Manager, Trader, and Portfolio Manager roles, along with persistent decision logging and checkpoint resume capabilities [README].

A less obvious but significant feature is the memory system. Each completed run appends to a decision log at ~/.tradingagents/memory/trading_memory.md. On subsequent runs for the same ticker, the system fetches realized returns (raw and alpha versus a benchmark), generates a one-paragraph reflection, and injects recent same-ticker decisions plus cross-ticker lessons into the Portfolio Manager prompt [README]. This is the framework’s attempt at learning from experience, though the authors candidly note that LLM-driven systems are inherently non-deterministic: identical ticker-date pairs can produce different outputs across runs due to model sampling and live data drift [README].

The Hype Cycle: From arXiv to GitHub Stardom

TradingAgents arrived at a receptive moment. The broader financial industry is in the midst of an agentic AI pivot. Moody’s reports that 70% of surveyed financial institutions prioritize AI for risk and compliance, with 66% seeking accelerated analysis and 64% cost reduction [8]. NASDAQ and other institutions are adopting agentic AI over traditional generative AI approaches [10]. NVIDIA has deployed its own multi-agent quantitative signal discovery system using the Nemotron model family and NeMo Agent Toolkit, automating the alpha research loop that was previously manual [12].

The project’s GitHub repository, maintained by Tauric Research, has accumulated significant attention—enough to warrant a star-history chart in the README and translations into eight languages [README]. The authors’ follow-up paper, “Trading-R1: Financial Trading with LLM Reasoning via Reinforcement Learning,” appeared in 2025 with a terminal implementation promised [README][9]. The original paper was selected for oral presentation at “Multi-Agent AI in the Real World” [5].

This attention reflects a broader shift in financial AI from isolated prediction tasks toward workflow-centric automation integrating planning, memory, and tool use [4]. TradingAgents sits at the intersection of two trends: the academic interest in multi-agent collaboration, and the practitioner’s hunger for systems that can explain why they bought what they bought.

What the Numbers Claim—and What They Hide

The authors assert that their multi-agent architecture achieves “notable improvements in cumulative returns, Sharpe ratio, and maximum drawdown” compared to baseline models [3][5][9]. These claims are presented without the granular backtest parameters—specific date ranges, transaction cost assumptions, slippage models—that would allow independent verification. The framework’s own documentation warns that “trading performance may vary based on many factors, including the chosen backbone language models, model temperature, trading periods, the quality of data, and other non-deterministic factors” [README].

This candor is refreshing but also revealing. The reproducibility section of the README dedicates considerable space to explaining why results vary: model sampling non-determinism, live data drift in news and social sources, and reasoning models’ inherent volatility [README]. The authors suggest lowering temperature and using non-reasoning models like GPT-4.1 for tighter reproducibility, which implicitly concedes that the more capable reasoning models produce less stable trading signals.

The framework is explicitly “designed for research purposes” and disclaims financial advice [README]. This is not mere legal hedging. The gap between a research scaffold and a production trading system encompasses execution infrastructure, market impact modeling, regulatory compliance, and the adversarial dynamics of real markets—none of which TradingAgents addresses.

The Competitive Landscape: Agents Everywhere

TradingAgents enters a crowded field. BloombergGPT and FinGPT represent domain-adapted language models for financial NLP [4]. FinBERT specializes in sentiment classification. TradingGPT and similar tools handle narrower tasks like report generation and forecasting [11]. NVIDIA’s quantitative signal discovery system automates alpha research with a three-agent loop (signal generator, code agent, evaluator) backed by structured operator libraries to prevent mathematical hallucinations [12].

What distinguishes TradingAgents is its organizational fidelity. Where NVIDIA’s system optimizes for signal discovery speed, TradingAgents optimizes for decision process transparency. The bull-bear researcher debate, the risk management checkpoint, the portfolio manager approval—these are not necessarily optimal for pure returns, but they produce an audit trail of who thought what and when. In an industry facing increasing regulatory pressure for explainability, this architectural choice may prove more durable than any Sharpe ratio claim [8].

The framework’s multi-provider support also reflects strategic positioning. By accommodating Chinese models (Qwen, GLM, MiniMax with dual-region endpoints) alongside Western providers, Tauric Research has built infrastructure that travels across geopolitical boundaries [README]. The v0.2.5 release added “non-US alpha benchmarks,” suggesting the authors recognize that US-centric backtests mislead global users [README].

Criticism, Limits, and the Theater of Collaboration

The most pointed critique of multi-agent financial systems is not technical but epistemological: does adding more LLM instances improve reasoning, or merely distribute hallucinations across a larger cast?

The OWASP GenAI Security Project’s Agentic Security Initiative identifies specific risks in multi-agent financial deployments: memory poisoning through malicious data injection into vector databases, tool misuse via deceptive prompts targeting payment APIs, and privilege compromise through weak permissions [6]. TradingAgents’ simulated exchange execution mitigates some execution-layer risks, but the framework’s reliance on live news and social sentiment sources creates attack surfaces that single-agent systems do not share.

Moody’s analysis of agentic AI in financial services emphasizes that governance frameworks must evolve to ensure auditability, compliance, and prevention of bias and hallucinations, requiring human-in-the-loop oversight and structured decision-tracking [8]. TradingAgents’ structured communication protocol and persistent decision log partially address this, but the framework stops at simulated execution—no real money, no real market impact, no real regulatory exposure.

The “bounded autonomy” thesis proposed by Hui Gong at UCL suggests that near-term financial AI will involve “supervised co-pilots, monitors, and constrained execution modules within human workflows” rather than fully autonomous agents [4]. TradingAgents’ architecture—with its explicit Portfolio Manager approval gate and Risk Management checkpoint—aligns with this vision, though the framework’s marketing materials sometimes imply greater autonomy than the code delivers.

Where This Goes Next

TradingAgents’ trajectory depends on whether its organizational metaphor proves scalable or merely picturesque. The v0.2.x release series has focused on infrastructure breadth—more providers, more languages, checkpoint resume, Docker support—rather than depth in any single market or strategy [README]. The promised Trading-R1 terminal, teased in January 2026, may signal a move toward reinforcement learning and more autonomous decision-making [README].

The unresolved tension is between the framework’s research origins and its open-source adoption. Academic papers can claim Sharpe ratio improvements on carefully selected backtests. Production trading systems must survive regime changes, liquidity crises, and adversarial market structure. TradingAgents’ memory system and reflection mechanism are early steps toward adaptive behavior, but the framework’s non-determinism—acknowledged as a feature of LLM research tools—becomes a bug when real capital is at stake.

For now, TradingAgents serves as a sophisticated sandbox for studying how multi-agent collaboration might structure financial decisions. Whether it becomes more than a sandbox depends on whether its authors—or its community of contributors—can bridge the gap between simulated trading floors and the unforgiving reality of live markets.

Sources

- Leveraging AI Multi-Agent Systems in Financial Analysis

- Trading using LLM agents : r/algorithmictrading - Reddit

- TradingAgents: Multi-Agents LLM Financial Trading Framework

- AI Agents in Financial Markets: Architecture, Applications ... - arXiv

- TradingAgents: Multi-Agents LLM Financial Trading Framework - arXiv

- Multi-Agent AI in Financial Sector - LinkedIn

- TradingAgents : Best AI Agent for Financial Trading - Medium

- Agentic AI in financial services | Moody's

- TradingAgents: Multi-Agents LLM Financial Trading Framework

- Agentic AI in Financial Services: Choosing the Right Pattern for Multi ...

- Your Guide to the TradingAgents Multi-Agent LLM Framework

- Automating and Optimizing Financial Signal Discovery with Multi ...