virattt/ai-hedge-fund

Famous investors reborn as LLM agents, still not trading

To explore AI-driven trading, it orchestrates a committee of LLM agents cast as famous investors who analyze stocks and generate orders that never reach a market.

Velocity · 7d

+32

★ / day

Trend

↘cooling

star history

What it does

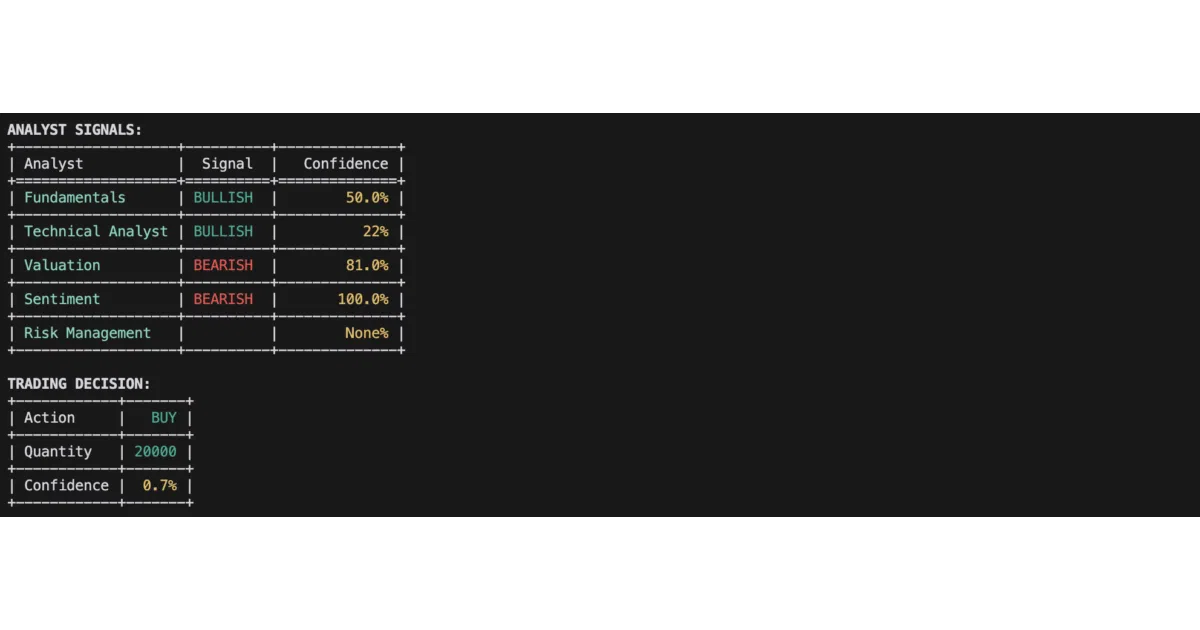

ai-hedge-fund is a Python simulation that models a hedge fund as a multi-agent system. Each agent adopts the persona of a legendary investor—Warren Buffett, Ben Graham, Cathie Wood, Michael Burry, and others—or performs a specific function like valuation, sentiment analysis, or risk management. A Portfolio Manager agent synthesizes their outputs into trading signals. The system includes a backtester and a web interface, but explicitly does not execute live trades.

The interesting bit The novelty is the Wall Street cosplay: the authors prompt LLMs to role-play as specific investors with distinct philosophies, from Graham’s margin-of-safety conservatism to Taleb’s tail-risk obsession. It is essentially a framework for prompting an LLM committee meeting where a risk manager and portfolio manager act as moderators. Whether this produces coherent strategy or just expensive fan fiction is left as an exercise for the user.

Key highlights

- 19 specialized agents, including named investor personas and functional analysts (valuation, sentiment, fundamentals, technicals).

- Requires external LLM and financial data APIs; supports local models via Ollama for the LLM layer.

- Includes a backtester and a web application for visualizing decisions.

- Explicitly educational: generates signals and orders but never connects to a brokerage.

- MIT licensed.

Caveats

- The README is clear that it does not execute trades, but it is vague on how the agent personas translate into reproducible, quantifiable edges versus stylized prompting.

- It relies on multiple paid third-party APIs (LLM providers and financial data), so running it is not free or fully offline even with Ollama.

- The educational disclaimer is prominent; anyone looking for an actual systematic trading engine will find a role-playing simulator instead.

Verdict Grab it if you want a sandbox for experimenting with multi-agent LLM architectures and financial prompting. Skip it if you are looking for a systematic, production-ready trading system or a fully offline stack.

Frequently asked

- What is virattt/ai-hedge-fund?

- To explore AI-driven trading, it orchestrates a committee of LLM agents cast as famous investors who analyze stocks and generate orders that never reach a market.

- Is ai-hedge-fund open source?

- Yes — virattt/ai-hedge-fund is open source, released under the MIT license.

- What language is ai-hedge-fund written in?

- virattt/ai-hedge-fund is primarily written in Python.

- How popular is ai-hedge-fund?

- virattt/ai-hedge-fund has 62.4k stars on GitHub and is currently cooling off.

- Where can I find ai-hedge-fund?

- virattt/ai-hedge-fund is on GitHub at https://github.com/virattt/ai-hedge-fund.