simonlin1212/TradingAgents-astock

Teaching a Multi-Agent Trader the Difference Between SPY and CSI 300

This fork rebuilds a popular multi-agent trading framework for the A-share market, replacing Yahoo Finance with free local data feeds and adding analysts who track policy shifts, hot-money flows, and lockup expirations instead of just fundamentals.

Velocity · 7d

+133

★ / day

Trend

↗accelerating

star history

What it does

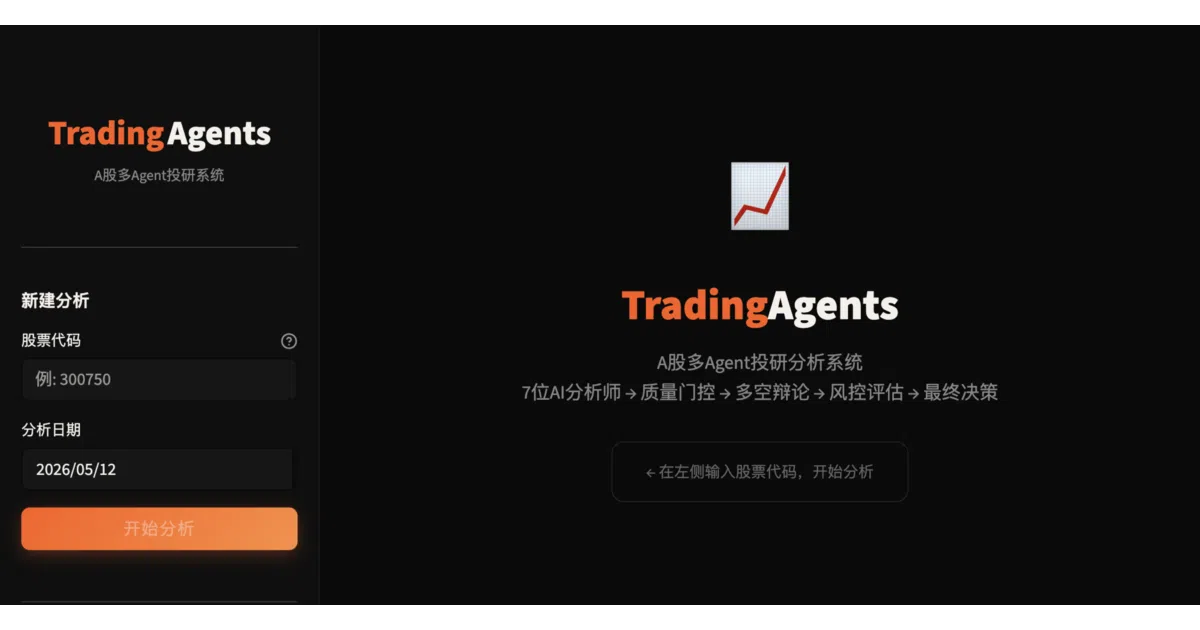

TradingAgents-astock is a specialized fork of the TradingAgents multi-agent research framework. It orchestrates seven AI analysts—market, sentiment, news, fundamentals, policy, hot-money, and lockup monitoring—whose individual reports feed into bull-versus-bear debates and a final portfolio manager that issues buy, hold, or sell decisions under A-share constraints like T+1 settlement, price limits, and lot sizing. All market data is pulled from free mainland sources such as mootdx, Tencent Finance, East Money, and Sina, with no API keys or credit walls required.

The interesting bit The project treats A-share adaptation as architectural surgery rather than translation. It adds three mainland-specific analyst roles—policy (监管 and industrial guidance), hot-money (龙虎榜 and 主力 flows), and lockup (解禁 and 减持 overhang)—because the upstream’s generic four-analyst setup would miss the drivers that actually move Chinese retail-heavy markets. The LLM strategy is also tiered: fast “quick-think” models handle the seven analysts and debaters, while heavier “deep-think” models are reserved for the research manager and portfolio manager nodes where synthesis matters.

Key highlights

- Seven specialized analysts, three of them A-share native: policy, hot-money flow, and lockup expiration monitors.

- Fully localized data layer:

mootdxTCP feeds, Tencent, East Money, Sina, Tonghuashun, Cailianshe, and Baidu—no Yahoo Finance, Alpha Vantage, or Tushare points required. - Trading logic respects A-share mechanics:

T+1, daily price limits, minimum lot sizes,STrules, and benchmarking against the CSI 300 instead ofSPY. - Dual-LLM design: cheaper fast models for research and debate, heavier models reserved for the two manager nodes that write the final investment plan.

- Built-in rate-limiting and Keep-Alive session reuse for East Money scraping to avoid IP bans during batch multi-agent runs.

Caveats

- Each stock analysis consumes 30–50 LLM API calls, so a paid API key is mandatory; subscription-tier chat accounts will not work.

- The README carries a standard “research and technical demonstration only” disclaimer, explicitly stating the output is not investment advice.

Verdict Worth a look if you are building quant research tools for mainland markets and want a ready-made multi-agent reasoning scaffold. Give it a pass if you need live trade execution—the project explicitly disclaims investment advice and is framed as a research demonstration, not a production trading system.

Frequently asked

- What is simonlin1212/TradingAgents-astock?

- This fork rebuilds a popular multi-agent trading framework for the A-share market, replacing Yahoo Finance with free local data feeds and adding analysts who track policy shifts, hot-money flows, and lockup expirations instead of just fundamentals.

- Is TradingAgents-astock open source?

- Yes — simonlin1212/TradingAgents-astock is open source, released under the Apache-2.0 license.

- What language is TradingAgents-astock written in?

- simonlin1212/TradingAgents-astock is primarily written in Python.

- How popular is TradingAgents-astock?

- simonlin1212/TradingAgents-astock has 2.7k stars on GitHub and is currently accelerating.

- Where can I find TradingAgents-astock?

- simonlin1212/TradingAgents-astock is on GitHub at https://github.com/simonlin1212/TradingAgents-astock.