microsoft/qlib

Microsoft's quant research stack now comes with an LLM agent

Qlib provides a full-stack ML pipeline for quantitative finance—from alpha research to order execution—and now plugs into an LLM agent to automate R&D.

Velocity · 7d

+37

★ / day

Trend

↘cooling

star history

What it does

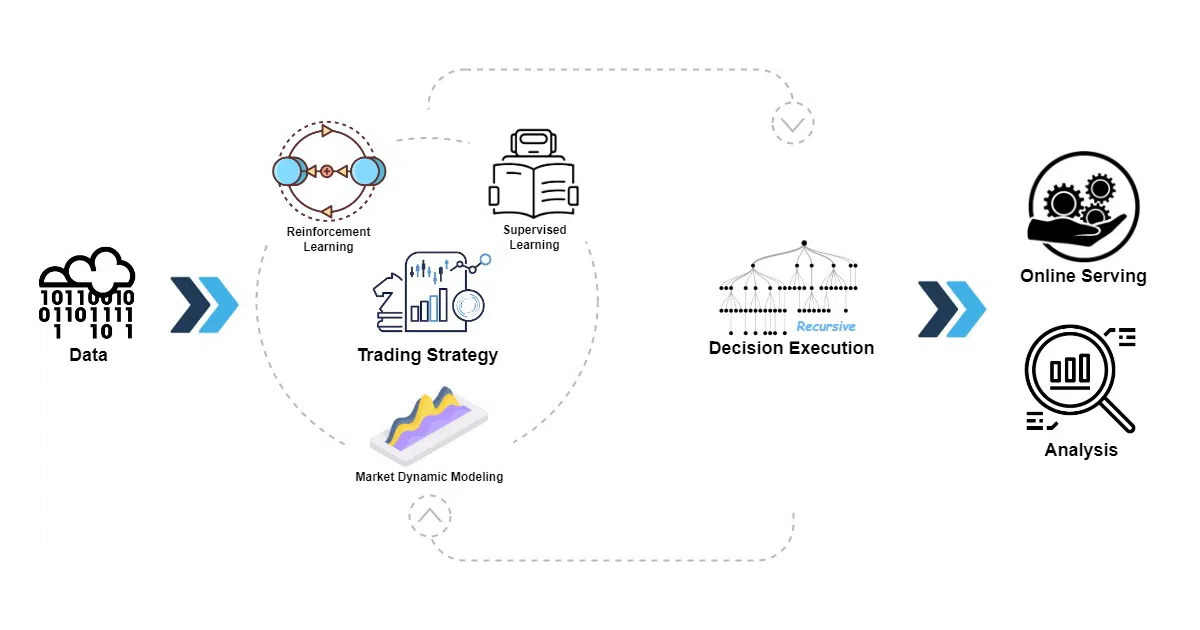

Qlib is an open-source Python platform for quantitative investment that covers the entire workflow: data processing, model training, back-testing, risk modeling, portfolio optimization, and order execution. It treats quant research as a modular ML pipeline where components like data providers, models, and execution strategies are loosely coupled. The project also integrates with Microsoft’s separate RD-Agent project to automate factor mining and model optimization using LLMs.

The interesting bit

Most quant libraries stop at back-testing; Qlib attempts to own the whole chain from signal generation to trade execution. It also doubles as a living repository of recent academic quant research, shipping implementations of papers like HIST, IGMTF, and KRNN alongside the infrastructure. The recent addition of LLM-driven agents suggests the maintainers want to automate not just execution but the research itself.

Key highlights

- Covers full quant lifecycle: alpha seeking, risk modeling, portfolio optimization, and order execution

- Supports diverse ML paradigms: supervised learning, market dynamics modeling, and reinforcement learning

- Modular, loosely-coupled architecture lets components be used standalone

- Ships with a “Quant Model Zoo” implementing recent SOTA research papers

- Now integrates with RD-Agent for LLM-based automated factor mining and model optimization

Caveats

- RD-Agent integration lives in a separate repository; it is not bundled natively

- Several advertised features (e.g., BPQP) are still under review or marked “coming soon”

- The documentation surface is sprawling, which may steepen the learning curve

Verdict

Worth a look if you are a quant researcher or data scientist who wants a unified Python stack for testing ML-driven strategies end-to-end. Skip it if you are looking for a simple trading bot or a lightweight back-tester—this is closer to a research operating system than a script.

Frequently asked

- What is microsoft/qlib?

- Qlib provides a full-stack ML pipeline for quantitative finance—from alpha research to order execution—and now plugs into an LLM agent to automate R&D.

- Is qlib open source?

- Yes — microsoft/qlib is open source, released under the MIT license.

- What language is qlib written in?

- microsoft/qlib is primarily written in Python.

- How popular is qlib?

- microsoft/qlib has 46.5k stars on GitHub and is currently cooling off.

- Where can I find qlib?

- microsoft/qlib is on GitHub at https://github.com/microsoft/qlib.