khuangaf/CryptocurrencyPrediction

A 2017 time capsule: predicting Bitcoin with Keras and Python 2.7

Student project compares LSTM, GRU, and 1D CNN on five-minute Poloniex tick data, finds deep learning barely beats linear regression.

Not currently ranked — collecting fresh signals.

star history

What it does

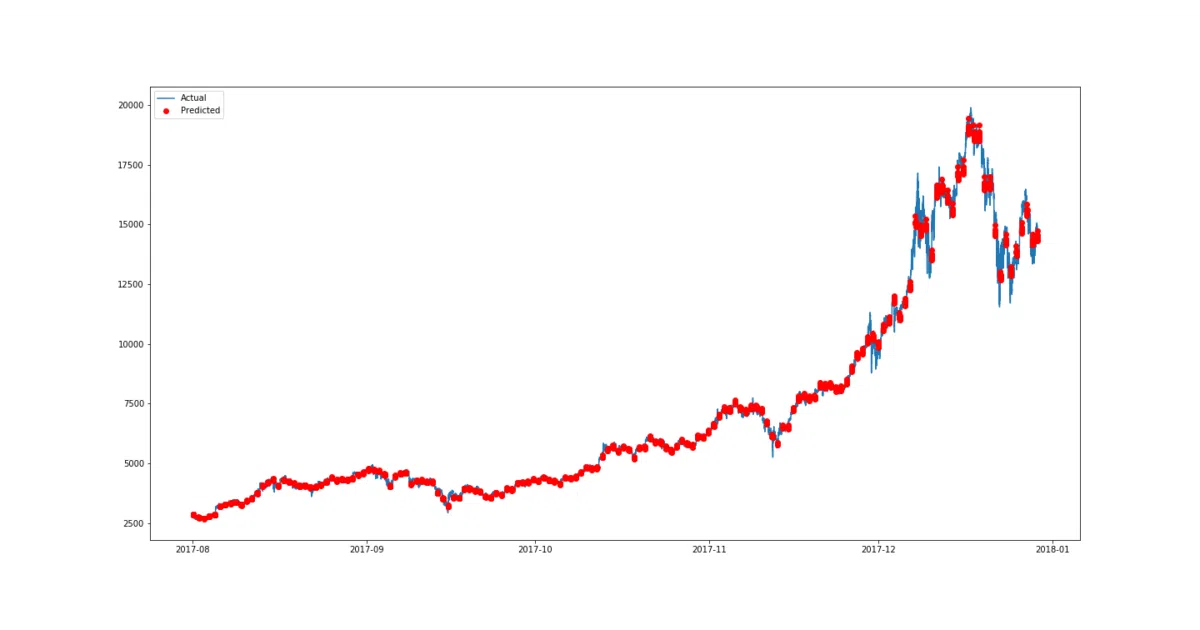

Trains LSTM, GRU, and 1D CNN models in Keras on 256-step windows of Bitcoin price data (five-minute ticks from Poloniex) to predict the next 16 steps—about 80 minutes ahead. The repo includes data collection notebooks, model scripts, and plotted validation results. It was built as a final-year project and the README frames it explicitly as a learning exercise.

The interesting bit

The results table is admirably honest: the best LSTM barely edges out a simple lag baseline and linear regression on test loss, and the author flags a likely bug in the 4-layer CNN that explodes validation loss to 12 million. That transparency is rarer than the “state-of-art” claim in the introduction suggests.

Key highlights

- Three model architectures: LSTM, GRU, and 1D CNN with configurable layers and activations

- Data pipeline from Poloniex → h5py via Jupyter notebooks (DataCollection.ipynb, PastSampler.ipynb)

- MinMax-scaled inputs, MSE loss, 100 training epochs per experiment

- Leaky ReLU consistently outperforms plain ReLU across architectures

- CNN trains fast (2 sec/epoch on GPU) but captures local temporal patterns less effectively than recurrent models

Caveats

- Frozen in 2017: requires Python 2.7, TensorFlow 1.2.0, and Keras 2.1.1—reproducing this today is archaeology, not engineering

- The “state-of-art” framing in the README is aspirational; the results show marginal improvement over trivial baselines

- No code for the regularization update mentioned at the bottom—only a notebook name, no file

Verdict

Worth a quick skim for students building their first financial time-series project and wanting a template for honest benchmarking. Anyone seeking profitable crypto prediction should look elsewhere—though they probably already knew that.

Frequently asked

- What is khuangaf/CryptocurrencyPrediction?

- Student project compares LSTM, GRU, and 1D CNN on five-minute Poloniex tick data, finds deep learning barely beats linear regression.

- Is CryptocurrencyPrediction open source?

- Yes — khuangaf/CryptocurrencyPrediction is open source, released under the MIT license.

- What language is CryptocurrencyPrediction written in?

- khuangaf/CryptocurrencyPrediction is primarily written in Jupyter Notebook.

- How popular is CryptocurrencyPrediction?

- khuangaf/CryptocurrencyPrediction has 1k stars on GitHub.

- Where can I find CryptocurrencyPrediction?

- khuangaf/CryptocurrencyPrediction is on GitHub at https://github.com/khuangaf/CryptocurrencyPrediction.