firmai/machine-learning-asset-management

Top-tier quant research that keeps its notebooks off-site

This repo catalogs the Python notebooks and data behind peer-reviewed research on machine-learning-driven portfolio construction, spanning roughly 15 trading strategy types and seven weight-optimization methods.

Not currently ranked — collecting fresh signals.

star history

What it does

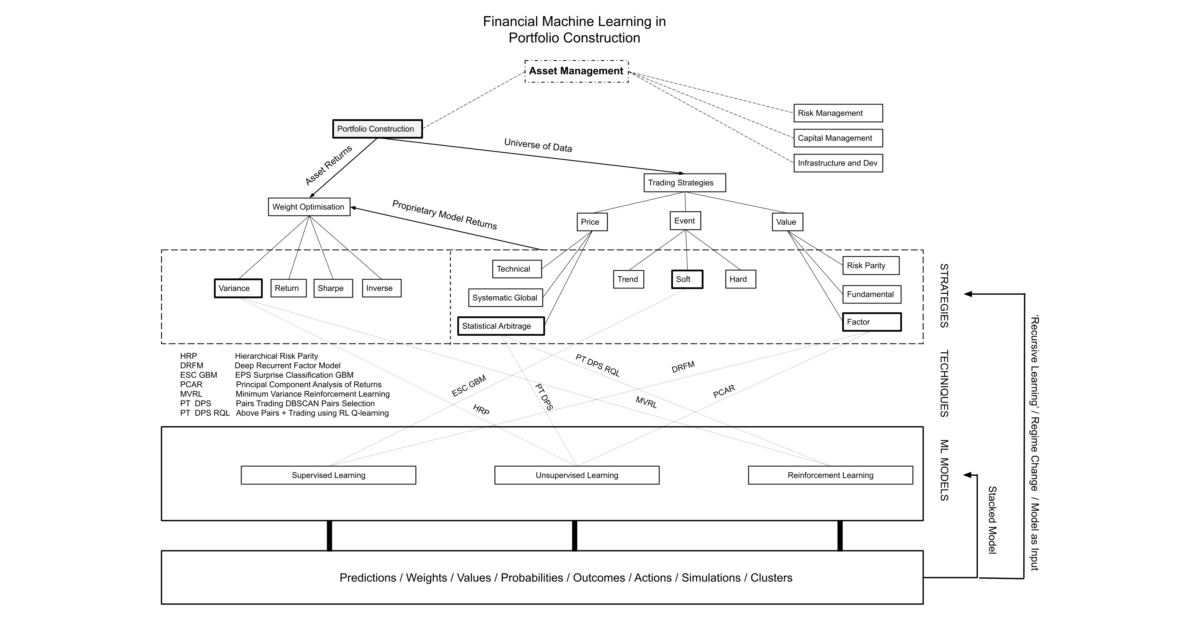

This repository serves as a curated companion to two Journal of Financial Data Science papers by Derek Snow, covering machine learning in portfolio construction. Part one links to resources for roughly 15 distinct trading varieties—ranging from Tiny CTA and reinforcement-learning agents to bankruptcy prediction and stacked ensembles—while part two catalogs seven weight-optimization approaches, including HRP, deep portfolios, and network-graph methods. Rather than hosting the bulk of the code directly, the README functions as a heavily annotated table of contents, pointing to Google Drive folders, Google Colab notebooks, and external repositories for data and implementation.

The interesting bit

The project treats academic rigor as a feature, not a bug: the underlying papers were edited by Marcos López de Prado and Frank J. Fabozzi, and the author claims top-1% SSRN download status across multiple categories. That makes this less a drop-in trading engine and more a structured literature review with executable sidecars.

Key highlights

- Companion to two JFDS papers split across trading strategies and weight optimization.

- Links to roughly 15 strategy archetypes (e.g.,

Tiny CTA,Quantamental,GANVaR) and around 100 trading strategies. - Weight-optimization section covers supervised, unsupervised, and reinforcement-learning frameworks.

- Curated by the FirmAI / ML Quant group, with additional related projects like

AtsPyandPandaPynoted. - Claims top-1% SSRN download rankings and all-time top-10 placement in several e-journal categories.

Caveats

- The GitHub repo itself is largely an index; most notebooks, data, and code reside on external Google Drive or Google Colab links.

- It is unclear from the

READMEwhich notebooks are stored in the repository versus hosted entirely off-site. - Some strategy descriptions are minimal—links to papers and external blogs do the heavy lifting.

Verdict

Worth bookmarking if you are a quant researcher or practitioner looking for a curated, academically grounded map of ML trading techniques. Skip it if you need a monolithic, clone-and-run backtesting framework.

Frequently asked

- What is firmai/machine-learning-asset-management?

- This repo catalogs the Python notebooks and data behind peer-reviewed research on machine-learning-driven portfolio construction, spanning roughly 15 trading strategy types and seven weight-optimization methods.

- Is machine-learning-asset-management open source?

- Yes — firmai/machine-learning-asset-management is an open-source project tracked on heatdrop.

- What language is machine-learning-asset-management written in?

- firmai/machine-learning-asset-management is primarily written in Jupyter Notebook.

- How popular is machine-learning-asset-management?

- firmai/machine-learning-asset-management has 1.7k stars on GitHub.

- Where can I find machine-learning-asset-management?

- firmai/machine-learning-asset-management is on GitHub at https://github.com/firmai/machine-learning-asset-management.