ZhuLinsen/daily_stock_analysis · 28 Jun 2026 · Feature

The 49,000-Star Retail Quant: Why a Chinese Stock Scraper Became GitHub’s Favorite Analyst

Vanessa Cho

Staff Writer

An open-source system turns LLM prompts and public market data into daily push notifications for retail traders across three continents.

ZhuLinsen/daily_stock_analysis

★50.6k stars Velocity · 7d +1001 ★/day ↗accelerating

star history

The Fork-First Phenomenon

Most GitHub repositories measure popularity in stars. For daily_stock_analysis, the telling metric is forks: more than 43,000 of them as of mid-2026, according to one tracker, against roughly 49,000 stars. That skew matters because the project is explicitly designed to be adopted by forking it. Users copy the repository, store API keys in GitHub Secrets, and let GitHub Actions run the analysis on a schedule. No server rental, no Docker daemon, no cron job on a Raspberry Pi under a desk. The repository becomes a personal analyst that wakes up every weekday at 18:00 Beijing time, scrapes A-share, Hong Kong, and U.S. market data, prompts a large language model, and pushes a formatted decision dashboard to WeChat Work, Feishu, Telegram, Discord, Slack, or email.

This zero-infrastructure deployment model is the primary reason for the hype. A Threads post highlighting the project distilled its appeal neatly: it builds a full pipeline that collects market data, analyzes stocks with LLMs, generates structured reports, and tracks insights over time. A YouTube video specifically markets the “zero-cost deployment” angle. The repository has also been featured by Trendshift and HelloGitHub, and a derivative skill based on its codebase has appeared on agent-marketplace explainx.ai, where it is packaged for Cursor and other AI coding agents. In a landscape where institutional terminals cost thousands of dollars per month, the idea that a fork and a few API keys can produce a daily briefing is understandably seductive, particularly for retail investors in mainland China who need simultaneous visibility into A-shares, Hong Kong listings, and U.S. ADRs.

A Glue-Code Orchestra, Not an Oracle

Strip away the badges and the project is, candidly, an elaborate integration layer. It does not train proprietary price-prediction models or discover novel alphas. Instead, it orchestrates a wide array of existing data providers—AkShare, Tushare, YFinance, TickFlow, Baostock, Pytdx, Longbridge—and funnels their outputs through an LLM prompt template. The model providers are equally eclectic: Anspire, AIHubMix, Gemini, Claude, DeepSeek, Qwen, and local Ollama instances are all supported. News and sentiment come from SerpAPI, Tavily, Bocha, Brave, MiniMax, SearXNG, and an optional social-sentiment feed for U.S. equities.

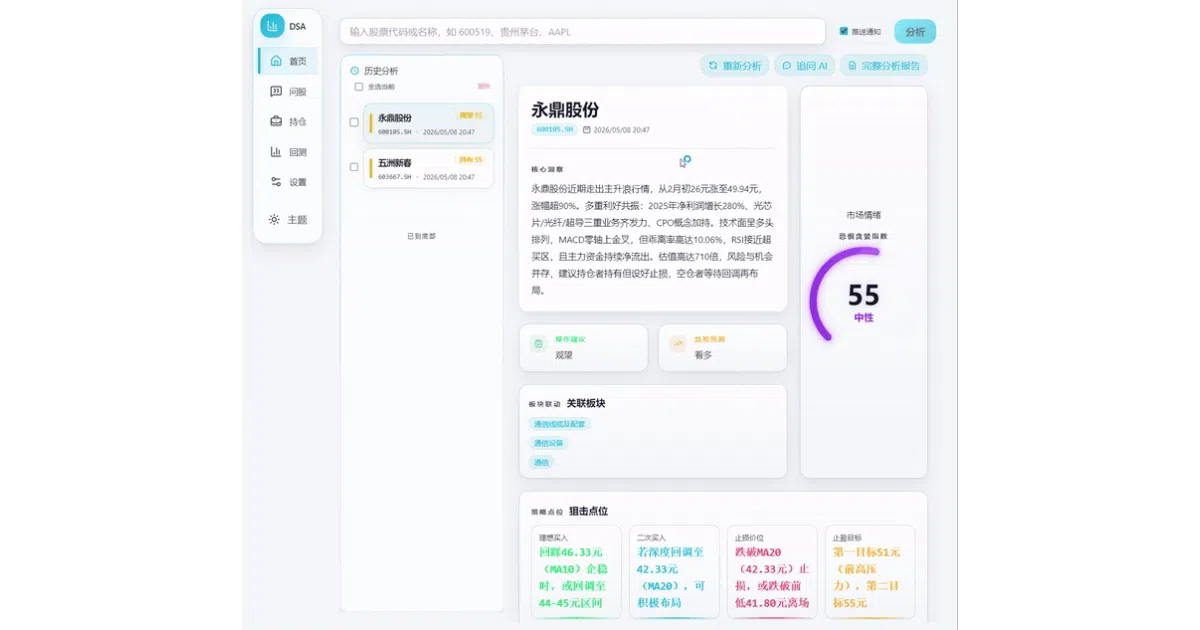

The value lies in the assembly. The system generates what it calls a “decision dashboard”: a structured report with core conclusions, numerical scores, trend labels, suggested buy and sell levels, risk alerts, catalyst summaries, and an operation checklist. A sample output shows a color-coded summary—green for buy, yellow for hold, red for sell—followed by bullet points on capital flow, chip concentration, and news sentiment, all timestamped and formatted for mobile chat apps. There is also a web-based workstation for manual analysis, historical report retrieval, backtesting, and portfolio tracking, complete with light and dark themes and smart import from images, CSVs, or clipboard snippets.

An “Agent strategy” chat mode allows multi-turn questioning using fifteen built-in templates: moving-average crossovers, Chanlun wave theory, Elliott Wave, trend-following, hot-theme tracking, event-driven logic, and growth-quality screens, among others. The agent can call live data during the conversation, export sessions, and even dispatch results to the same notification channels used by the daily batch job. The architecture is modular enough that the author has spun off two sibling projects: AlphaSift for multi-factor stock screening and AlphaEvo for strategy backtesting and self-evolution, suggesting ambitions to cover more of the quant pipeline than just daily commentary.

In that sense, the repository is a practical, retail-grade instantiation of the trend described in a March 2025 survey on AI in quantitative investment: the shift from deep-learning prediction toward LLM-powered agents that process unstructured data and support iterative workflows. It is not the only such instantiation, but it is among the most accessible.

The Retail Quant Stack

To understand where this project sits, compare it with the alternatives. At the institutional end, Reflexivity—built by former Lombard Odier portfolio managers—offers a SOC 2 Type 2 audited platform with LSEG Datastream, S&P Global fundamentals, knowledge graphs, and explicit “no hallucination” engineering. It is software for firms that manage billions. daily_stock_analysis is software for individuals who want a push notification before dinner.

Closer to its weight class, no-code workflow platforms like n8n offer templates that perform a similar trick: pull technical indicators and news, pass them to GPT-4o, and email an HTML report. One such template even handles right-to-left Hebrew formatting, illustrating how localized the personal-finance-automation niche has become. The difference is that daily_stock_analysis is code-first, China-market-native, and far more aggressive about data-source redundancy. It also predates or parallels the multi-agent fashion: a CrewAI-based stock-analysis platform described in a separate deep-dive uses specialized agents for research, technical analysis, and risk assessment, but targets Indian equities via Streamlit. daily_stock_analysis opts for a simpler monolithic prompt strategy, with experimental multi-agent support, and targets the Chinese-speaking retail trader first.

The project also fits into a broader open-source ecosystem clustered around the LLMQuant community, which maintains data-mcp servers, quant wikis, and curated lists of trading agents such as Magents and awesome-trading-agents. That community’s emphasis is on bringing LLM-native tooling to quantitative finance. daily_stock_analysis is arguably the most popular end-user application to emerge from that cultural moment: less a research framework, more a finished appliance that happens to be open source. The academic survey on AI in quant finance notes that LLMs have shown “remarkable power in understanding contextual data, generating accurate interpretations, and reasoning like human analysts.” This repository tests that claim at consumer scale, using off-the-shelf models to mimic the morning note of a human broker.

Where the Insight Ends

For all its plumbing excellence, the repository has hard boundaries. It is an analysis assistant, not a trading system. The README carries a standard but clear disclaimer: the outputs are for learning and research, not investment advice, and the author assumes no liability for losses. That is not mere legal hedging; it reflects the project’s actual capability. It generates narratives and scores, not executable orders.

The quality of those narratives is entirely hostage to the LLM and data sources chosen by the user. Unlike Reflexivity, which advertises institutional data contracts and auditable source tracing, this project relies on a mix of free-tier and commercial APIs with varying latency and coverage. If the model hallucinates a catalyst or misreads a technical indicator, the dashboard will look just as confidently formatted. The agent features, including multi-agent orchestration, are marked experimental. And while the project can backtest, it does not claim to have discovered durable alpha; it summarizes what others have already priced into the market. In the language of the quant survey, it sits at the “data processing” and “model prediction” stages of the alpha pipeline, with no bridge to portfolio optimization or order execution.

In practice, the “zero-cost” label applies only to compute. Users still feed metered LLM tokens and commercial data APIs into the pipeline. A heavy watchlist analyzed daily with multi-turn agent queries can rack up non-trivial inference costs. The economics are favorable compared to an institutional terminal, but they are not zero. These limitations do not negate its usefulness. They simply define it. The repository occupies a specific niche: the pre-trade research layer for retail investors who want structured daily commentary without manually tabbing between a charting site, a news feed, and a brokerage app. In doing so, it illustrates a wider shift in quantitative finance—one where LLMs are not replacing quants, as a LinkedIn discussion noted, but augmenting access to data and communication efficiency for everyone else. Whether that fork count translates into outperformance is, of course, a question the repository wisely leaves unanswered.

Sources

- From Deep Learning to LLMs: A survey of AI in Quantitative Investment

- Automated stock analysis reports with technical & news sentiment ...

- Zero-cost deployment of an AI trading analyst! daily_stock_analysis ...

- AI and LLMs in finance: enhancing efficiencies and communication

- Reflexivity - Investment Analysis Platform

- Automate your daily stock research with AI. - Threads

- LLMQuant - GitHub

- I've built an automated research agent for stock analysis - Reddit

- Complete Guide to the AI Stock Analysis Tool 2026 - Tosea.ai

- Spring 2026 | Applications of LLMs and AI in Quantitative Finance

- Building an AI-Powered Stock Analysis Platform: A Deep Dive into ...

- stock-daily-analysis — AI agent skill - explainx.ai